Deciding what to do with the family home is often the largest financial decision you will face during a divorce. Emotions run high, but protecting your financial future should come first. With specialized expertise in divorce real estate, we provide the objective, data-driven guidance you need to evaluate your options without taking sides.

The Four Paths for the Marital Home

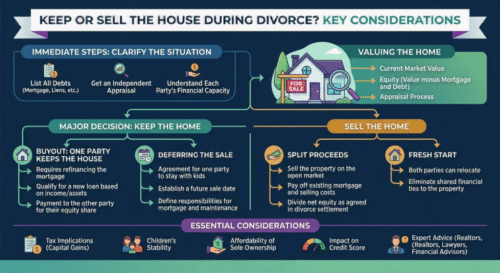

When dividing a real estate asset in a divorce, you generally have four choices:

1. Immediate Sale and Division of Proceeds – Selling the property is often the cleanest way to achieve a fresh start.

The Pros: It completely severs the financial tie between spouses, releases cash equity, and provides clear boundaries.

The Cons: Both parties must relocate, which can disrupt children’s school schedules and routines.

2. One Spouse Buys Out the Other – One spouse takes full ownership of the property by paying the departing spouse their share of the home’s equity.

The Pros: Minimizes disruption for children and allows one party to stay in a familiar neighborhood.

The Cons: Requires the staying spouse to qualify for a new mortgage entirely on their own income.

3. Deferred Sale (Co-Ownership) – Both spouses remain on the deed and mortgage for a specified period (e.g., until the youngest child graduates), after which the home is sold.

The Pros: Delays relocation during a sensitive time for the family.

The Cons: Keeps your credit tied to your ex-spouse. If they miss a payment, your credit score suffers.

4. Property Trade-Off – One spouse keeps the house, while the other receives assets of equal value, such as retirement accounts, investments, or other vehicles.

The Pros: Avoids the need to refinance the home immediately.

The Cons: Real estate is an illiquid asset with ongoing maintenance costs, whereas retirement accounts carry different tax implications.

Key Financial Factors to Consider

Before making a final decision, look past the emotional attachment to the property and calculate these three realities:

A. The True Cost of Ownership – Can a single income cover the mortgage, property taxes, insurance, utilities, and emergency repairs?

B. Capital Gains Taxes – The IRS allows a $500,000 exclusion on capital gains for married couples selling a primary residence, but only $250,000 for single filers. Timing your sale matters.

C. Current Market Conditions – Interest rates and local inventory will dictate how quickly your home sells and how much equity you will actually walk away with.

Get a Neutral, Expert Assessment

Don’t guess the value of your home or rely on automated online estimates during a legal proceeding. We provide court-ready property valuations to help you and your legal team make the right choice.

Request a Confidential Consultation

Learn More: The Spouse Buyout Guide, Frequently Asked Questions, California Courts Self-Help Guide